By Calum MacRae, Director, Supply Chain & Technology,

S&P Global Mobility

With energy prices in Europe skyrocketing, placing business

bottom lines in triage mode, a harsh winter could place certain

automotive sectors at risk of being unable to keep their production

lines running.

The combined black swan events of the COVID-19 pandemic and the

Russian invasion of Ukraine have already stretched the automotive

supply line – especially in regard to semiconductors. Now, some

OEMs and suppliers with energy-intensive manufacturing processes

may face extensive pressure in terms of energy costs in the coming

months.

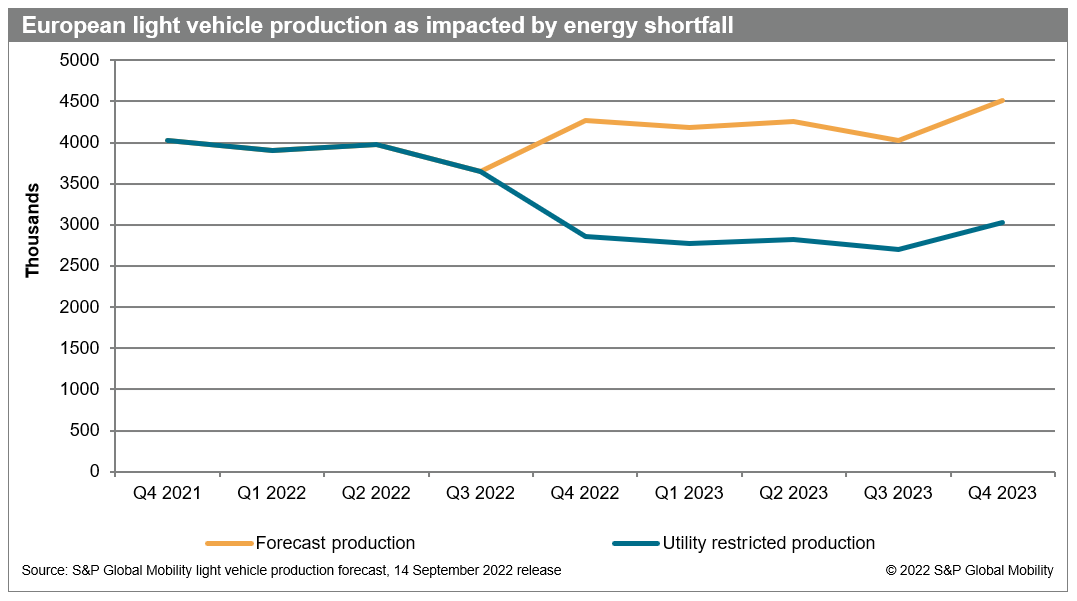

As a result, potential manufacturing losses from Europe-based

OEM final-assembly plants could reach more than 1 million units per

quarter, starting in the fourth quarter of 2022 through the

entirety of 2023, according to forecasts by S&P Global Mobility

and S&P Commodity Insights.

Starting in the fourth quarter of 2022 through 2023, quarterly

production from Europe-based auto manufacturing plants was forecast

to be in the 4-4.5-million-unit range per quarter – predicting

moderate growth. However, with potential utility restrictions, that

OEM output could be reduced to as low as 2.75-3 million units per

quarter.

As seen with past regional events – Ukraine-sourced neon

shortages hampering semiconductor deliveries, and the 2011 Japan

earthquake and tsunami crippling supplies for microcontrollers,

mass-airflow sensors, and Xirallic paint pigments – losing one

crucial piece in the global supply chain can bring the automotive

manufacturing industry to a crunching halt.

The consensus forecasts for a cold, wet European La Niña winter,

combined with energy shortages, could have a similar effect. The

recent leaks in the subsea Russian pipelines to Europe adds to risk

and the likelihood that our model is directionally correct.

S&P Global Mobility is forecasting significant supply chain

disruption from November through spring. We also anticipate

disruption of the traditional just-in-time supply model due to some

suppliers implementing a schedule of working fractional-months on a

24/7 setup – which can be more energy-efficient than traditional

weekly shifts due to the latter’s higher start-up and shut-down

energy costs.

We consider mandatory energy rationing to be the basis for a

pessimistic scenario for the region’s auto producers and suppliers.

For an industry already struggling with low inventories of vehicles

in dealer showrooms, an additional crisis could be incapacitating

on a global scale.

European suppliers send parts, components, and modules to OEMs

around the world – thus impacting all automakers, not just regional

ones. And U.S. retail customers could also suffer, as EU/UK

manufacturing plants are currently exporting about 7,000 units per

month to American shores – but shipped 213,750 vehicles in the

entirety of 2019, according to Global Trade Atlas.

“If you look through the supply chain – particularly where

there’s any metallic structure forming through pressing, welding or

extrusion – there’s a tremendous amount of energy involved,” said

Edwin Pope, Principal Analyst, Materials & Lightweighting at

S&P Global Mobility. “Total energy usage in these companies

could be up to one-and-a-half times what we’re seeing in vehicle

assembly today. Anecdotally, we’re hearing that some of this

manufacturing capacity is becoming so uneconomic that companies are

simply shutting up shop.”

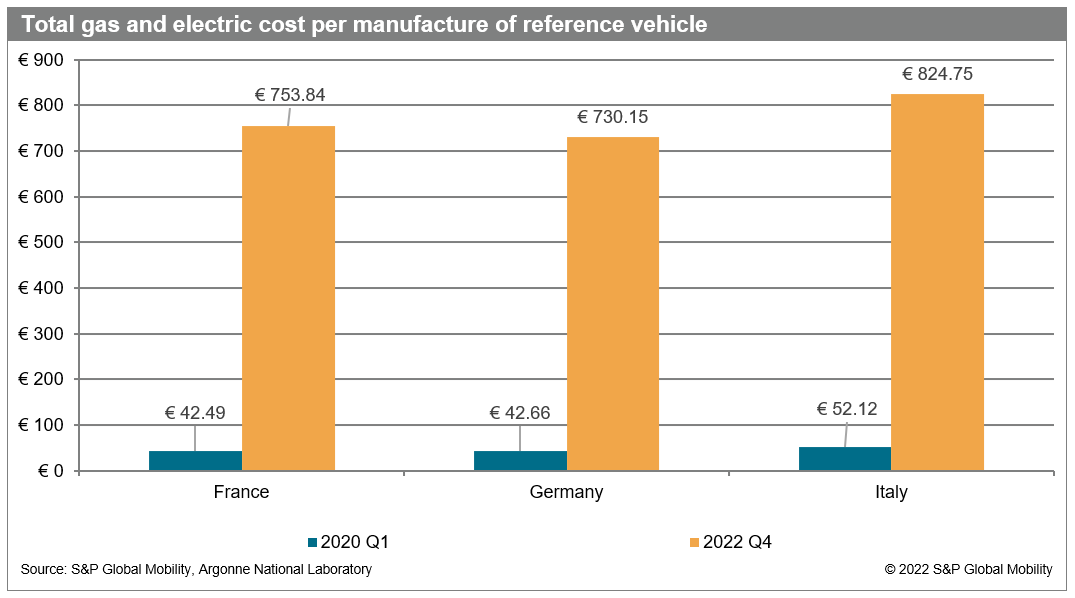

Before the energy crisis, gas and electric costs were a

relatively inconsequential component of a vehicle’s bill of

materials, typically less than €50 per vehicle. Now with cost

increases ranging from €687 to €773 per vehicle, energy costs

compound an already perilous position for the sector – given the

impact raw material price increases have already had on the nascent

electric vehicle value chains. Both serve to undermine margins in a

market where cost increases will be difficult to pass on to

customers already facing food and energy inflation.

Across the European Union, energy constraints could result in

nations or regions enacting emergency policies to counter this

threat. OEMs also have a certain level of countervailing power with

the regional utility companies and via governmental lobbying

operations.

“However, the pressure on the automotive supply chain will be

intense, especially the more one moves upstream from vehicle

manufacturing,” Pope said. “Upstream supplier parts production

constraints could impact OEM volumes. As a result, we see a risk of

OEMs halting shipments of completed vehicles due to shortages of

single components, which are not necessarily coupled to

country-level energy policies.”

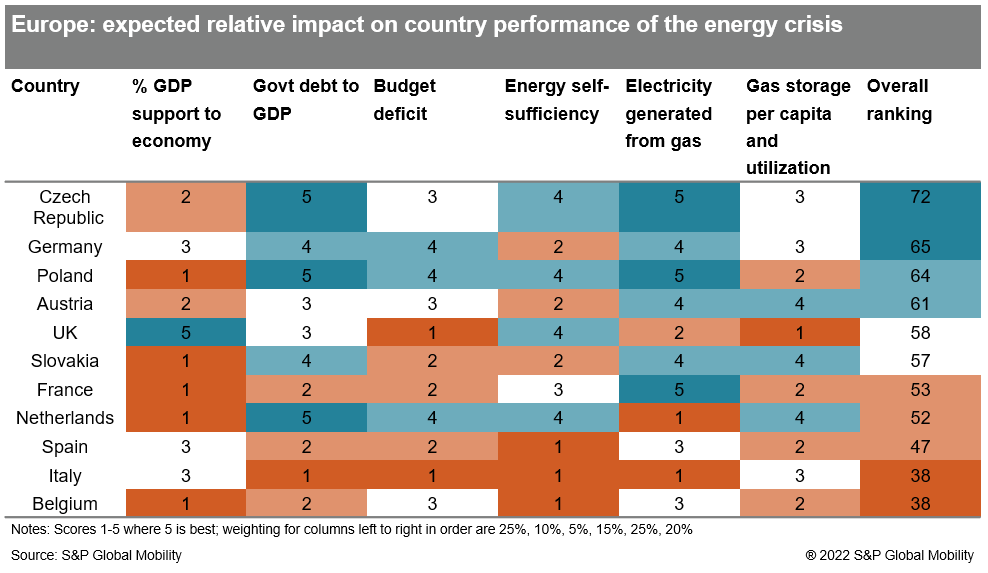

How countries will be able to react

S&P Global Mobility has modeled the impact of the looming

energy crunch on 11 European countries – each a significant vehicle

production location – to assess which countries’ automotive

segments are best positioned to withstand the severe energy

headwinds this winter.

The model borrows from macroeconomic aggregate demand frameworks

in assessing consumption, investment, and government expenditure to

which an assessment of energy mix and gas storage is added. Based

on a quantitative assessment of available information, six

dimensions are scored on a relative basis between 1 and 5, with 5

being the best score.

The effect the energy crisis could have on a country’s economic

performance and societal wellbeing can also be connected to a

country’s industrial footprint. The most energy intensive

industrial sectors are aviation and shipping, but their energy

consumption is tied almost exclusively to oil, where price

increases have not been of the magnitude seen in gas and

electricity. Industrial sectors that see high usage of gas and

electricity include chemicals and metallic products, both of which

are intrinsically tied to automotive manufacturing.

Individual countries’ policy responses in addressing energy

imbalances will also impact comparative economic performance. Such

policies will determine how a country’s energy mix impacts the

comparative advantage of vehicle build locations in Europe.

That impact is shown by some counterintuitive results in the

S&P Global Mobility analysis. Germany has relied on Russia for

its gas supplies and is phasing out nuclear power, both of which

would seem to place that nation in a precarious energy situation.

However, Germany benefits from its government’s famous fiscal

rectitude, which gives it relatively more budgetary headroom to

ride out the energy storm. Further, the country benefits from a

relatively low reliance on electricity generation derived from gas

and from being in a decent position from a gas storage

perspective.

The model also reveals how crucial government intervention in

household and industry support has been for the UK. In the past few

weeks, the UK government has announced measures adding up to some

GBP200 billion for consumers and industry – accounting for nearly

7% of the country’s GDP and more than double the level of its

nearest rival Italy. Without such support, the UK would be near the

bottom of the table, in a position similar to that of Italy – which

suffers doubly owing to its debt and budget deficit position as

well as its low energy self-sufficiency and reliance on gas power

for electricity generation.

The chart also brings into focus the relative position of a

country’s macroeconomic position vis-à-vis energy and macroeconomic

policies. Italy is one of the more vulnerable economies, and this

weakness will be further compounded by the relative cost

disadvantage its manufacturing base faces.

Not all countries will be impacted equally by the energy market

imbalances roiling markets in Europe. That said, it is clear that

an era of abundant, and cheap, energy is over – and this has

shocked policymakers into varying degrees of response.

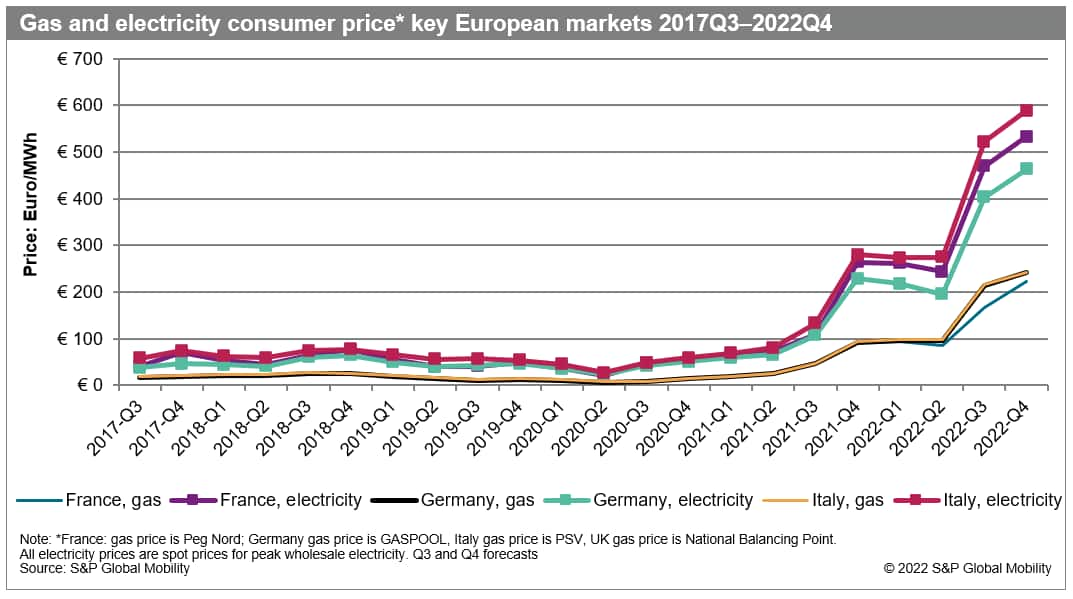

The impact of energy prices

Since first quarter 2020, energy prices in Europe have soared.

According to S&P Global Mobility data for four key markets –

Italy, Germany, France and the UK – gas prices have increased by an

average of 2,183%, a factor of nearly 23. The wholesale electricity

price increased by an average of 1,230% or a factor of more than

13.

The impact of the surge in prices is shown starkly in the

subsequent chart. Applying energy prices from the start of 2020 and

comparing with the current situation permits a view of the

additional cost that has been borne by OEMs. The subsequent chart

shows the gas and electricity cost increase for a typical reference

vehicle across France, Germany, and Italy.

For high-energy intensity sectors like automotive manufacturing,

S&P Global Mobility has developed a methodology, leveraging

proprietary data assets, to estimate the impact on vehicle

manufacturing’s bottom line due to escalating energy costs.

To allow for an apples-to-apples comparison in examining typical

energy usage in each stage of final assembly, the single reference

vehicle used was a Volkswagen Golf MKVIII, tipping the scales at a

shade under 1,370 kg, and considering local energy mix.

There are some caveats to this methodology. Carmakers sometimes

source their energy with different mixes than the country where

they operate, while we assume identical energy sourcing in our

model. Automakers also tend to lock gas and electricity prices with

utilities and use different financial instruments to reduce their

exposure – to the point they often end up reporting significant

windfalls from these hedging bets, as seen recently with the likes

of Volkswagen and Daimler. In our model, we assume they are paying

wholesale spot prices.

Ominous signs for the supplier tiers

Despite these warning signs, some OEMs protect their supplier base

by indexing the price of key commodities monthly for their

suppliers, which means that some suppliers are not locked into

contracts at an inelastic price point through the length of the

contract. However, this practice is not completely widespread.

“As you go further upstream, the sheltering the OEM provides

becomes less,” Pope said. “Additionally, smaller companies in Tiers

2 and 3 of the supply chain are likely to neither have the

resources nor the operational sophistication required for hedging

instruments, forward contracts and the like.”

The situation Europe faces may be only transient. Much will

depend on how the Russia-Ukraine conflict unfolds. However, a

longer-term transformation of the energy picture could result in

structural consequences for the industry. This would see production

schedules, manufacturing footprints and sourcing strategies being

discarded and replaced with a shift to locations where the energy

cost burden is least. While Europe faces a winter of discontent

now, more disruption could follow. This will bring fundamental

upheaval to the region’s auto sector and beyond.

In the way that labor cost used to be a key determinant of

manufacturing location, energy mix and self-sufficiency could

become key elements of future sourcing decisions.

This article was published by S&P Global Mobility and not by S&P Global Ratings, which is a separately managed division of S&P Global.

More Stories

Lewis Hamilton Shows Off New Helmet for Monaco GP by Daniel Arsham

Son parte de Star Wars los dos VW ID. Buzz muy especiales, e inspirados en “Obi-Wan Kenobi”

2022 Audi Q5 Sportback Review: Rounding out the top